Access the eBook here: Q1 2026 Corporate Immigration Updates

Cross-border remote work compliance has rapidly evolved from a niche HR concern into a core enterprise risk function. What was once treated as an employee perk—working from another country for a few weeks or months—now sits at the intersection of some of the most complex legal and regulatory frameworks global businesses must navigate.

The shift didn’t happen overnight. It accelerated quietly as distributed work became normalized, but regulators have now caught up. The OECD’s January 2026 consultation made one thing unmistakably clear: cross-border remote work is no longer a grey area—it is a structured compliance challenge requiring coordinated oversight across tax, labour law, immigration, payroll, and social security systems.

At the heart of the issue lies fragmentation. Each jurisdiction applies its own thresholds for tax residency, employer obligations, permanent establishment risk, and worker protections. When employees split time between countries—or relocate without formal assignment structures—companies can inadvertently trigger corporate tax exposure, create payroll liabilities, or violate local employment laws without even realizing it.

For example, a single employee working remotely from another country may:

-

🔸Create a permanent establishment (PE) risk under OECD Article 5

-

🔸Trigger local payroll withholding obligations

-

🔸Fall under mandatory employment protections in the host country

-

🔸Require immigration authorization, even for short stays

-

🔸Lead to double social security contributions in the absence of treaties

These risks are not theoretical. Tax authorities are increasingly scrutinizing remote work patterns, and enforcement is becoming more data-driven. At the same time, businesses are struggling to keep up with inconsistent rules and lack of global harmonization.

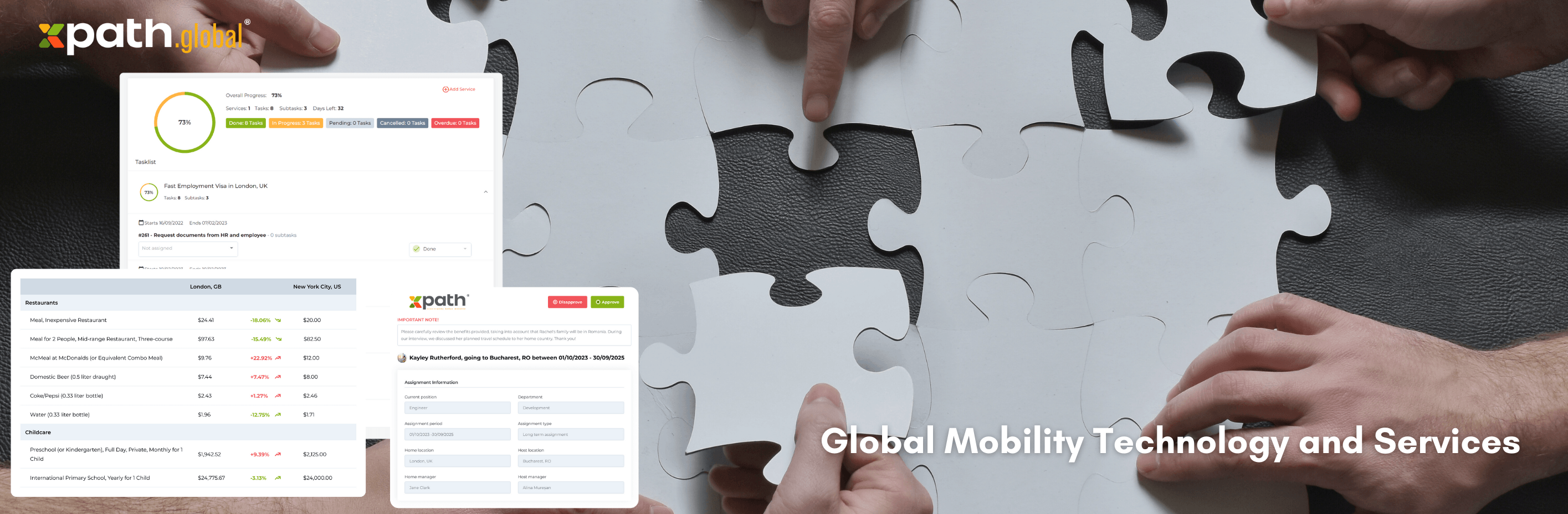

This is where structured solutions and advisory frameworks become essential. Platforms like (xpath.global) are emerging to help organizations centralize risk assessments, monitor employee location data, and align compliance across jurisdictions—bridging the gap between policy and execution.

Ultimately, the challenge is no longer whether companies allow cross-border remote work—it’s whether they can control the legal and tax consequences that come with it.

In this guide, we’ll break down the legal foundations, regulatory risks, and 10 powerful strategies for cross-border remote work compliance—giving you a clear, actionable framework to operate confidently in this increasingly complex global environment.

Cross-Border Remote Work Compliance

At its core, cross-border remote work compliance refers to the obligation of employers to manage and adhere to overlapping legal and regulatory requirements when employees perform work outside their primary country of employment—whether temporarily or on an ongoing basis. While the concept sounds straightforward, its execution is anything but. The complexity arises from how different jurisdictions interpret “work,” “presence,” and “economic activity,” often leading to unintended legal exposure.

A critical starting point is distinguishing between business travel, formal assignments, and remote work arrangements. Traditional business travel—short-term visits for meetings or conferences—has long benefited from clearer thresholds and exemptions under tax treaties and immigration rules. However, remote work blurs these boundaries. An employee working from a foreign jurisdiction, even without client interaction or revenue generation, may still create tax nexus, employment rights, or regulatory obligations for the employer.

From a legal standpoint, the concept of nexus becomes central. Nexus determines whether a country has the right to tax income or impose regulatory obligations on a business. In cross-border remote work scenarios, nexus can be triggered not by corporate presence, but by individual employee activity. This marks a significant shift from traditional models of international business, where physical offices or subsidiaries were the primary triggers.

The situation becomes even more intricate when considering the interaction of multiple legal regimes. Cross-border remote work compliance does not sit within a single legal domain—it operates at the intersection of:

-

Corporate tax law (permanent establishment, profit attribution)

-

Individual income tax law (residency, source taxation)

-

Payroll and withholding regulations (employer obligations in host country)

-

Labour and employment law (mandatory protections, termination rules)

-

Immigration law (right to work, visa requirements)

-

Social security systems (contribution obligations and treaty coordination)

Each of these regimes applies its own tests and thresholds, and critically, they do not align. For instance, an employee may not trigger tax residency in a host country but could still fall under local labour protections. Similarly, immigration authorities may consider remote work as “work activity” requiring authorization, even if no local employer exists.

This fragmentation creates a compliance environment where partial compliance is effectively non-compliance. Companies cannot afford to assess risks in isolation—addressing tax exposure without considering employment law or immigration requirements leaves significant gaps.

Adding to the complexity is the increasing role of digital presence and economic substance. Authorities are moving beyond physical infrastructure and focusing on where value is created. If key decision-making or revenue-generating activities are performed remotely from another jurisdiction, regulators may argue that the company has established a sufficient presence to justify taxation or regulation.

To manage this effectively, organizations are turning to centralized solutions that integrate legal, tax, and HR data. Platforms like xpath.global provide structured frameworks for assessing jurisdictional risk, tracking employee location patterns, and aligning compliance strategies across multiple legal domains—transforming what would otherwise be a reactive process into a proactive governance model.

Ultimately, defining cross-border remote work compliance is not about a single rule or threshold. It is about understanding how multiple legal systems simultaneously assert jurisdiction over a single employee’s activity—and building the internal capability to manage that complexity in real time.

Corporate Tax Exposure and Permanent Establishment Risk in Cross-Border Remote Work Compliance

One of the most significant and often underestimated risks in cross-border remote work compliance is the potential creation of a permanent establishment (PE). Under OECD Model Tax Convention Article 5, a PE generally arises when a company has a fixed place of business through which its activities are wholly or partly carried on. Traditionally, this meant offices, branches, or factories. However, remote work has fundamentally disrupted this framework.

A key issue is whether a home office can constitute a fixed place of business. Tax authorities increasingly examine whether the employer has “disposal” over the location. While occasional remote work may not meet this threshold, repeated or structured arrangements—especially where the employee’s role is integral to the business—can shift the analysis. If the employee is effectively operating from a foreign jurisdiction on a sustained basis, authorities may argue that the company has established a taxable presence there.

Beyond fixed place PE, dependent agent PE (DAPE) risk is also highly relevant. If an employee habitually concludes contracts or plays a principal role in their conclusion, this may trigger PE status—even without a physical office. This is particularly concerning for senior executives, sales personnel, or individuals involved in strategic decision-making while working remotely across borders.

Once a PE is established, the next challenge is profit attribution. Under OECD guidance, profits must be allocated based on functions performed, assets used, and risks assumed—often referred to in connection with DEMPE (Development, Enhancement, Maintenance, Protection, and Exploitation of intangibles). Remote workers performing key functions in another jurisdiction can shift profit allocation in ways that significantly increase corporate tax exposure.

Complicating matters further, different jurisdictions apply inconsistent interpretations of PE thresholds. Some countries adopt a stricter stance on home office arrangements, while others focus more on economic substance. This lack of harmonization creates uncertainty and increases the risk of double taxation.

To mitigate these risks, companies are increasingly adopting structured compliance frameworks supported by tools such as https://xpath.global/, which allow organizations to assess PE exposure based on employee activity, duration of presence, and functional role. Without such frameworks, businesses risk unintentionally creating taxable footprints in multiple jurisdictions—often without the infrastructure to manage them.

Payroll Withholding and Individual Tax Obligations

Managing payroll in the context of cross-border remote work compliance is one of the most operationally complex challenges employers face. Unlike corporate tax exposure, which may develop over time, payroll obligations can arise immediately upon employee presence in a foreign jurisdiction.

Most countries impose withholding obligations on employers when employees perform work within their territory. This means that even short-term remote work can trigger requirements to register as an employer, operate local payroll, and remit income taxes to local authorities. The thresholds for these obligations vary widely—some jurisdictions impose them from day one, while others allow limited exemptions.

A particularly complex mechanism is shadow payroll. In cases where employees remain on home-country payroll but are working abroad, employers may need to run parallel payroll systems to ensure compliance with host-country tax reporting requirements. This creates administrative burden and increases the risk of errors, especially when dealing with multiple jurisdictions simultaneously.

Another layer of complexity arises from individual tax residency rules. Employees working remotely across borders may inadvertently become tax residents in more than one country, depending on factors such as days of presence, center of vital interests, or habitual abode. While tax treaties aim to resolve dual residency through tie-breaker rules, the process is not always straightforward and can lead to disputes.

Additionally, double taxation risks emerge when withholding obligations are triggered in one country while tax liabilities remain in another. Although foreign tax credits and treaty relief mechanisms exist, they often require precise documentation and timely reporting—areas where compliance gaps frequently occur.

From an employer perspective, the challenge is not just technical—it is also data-driven. Accurate tracking of employee location, duration of stay, and work activity is essential to determine when payroll obligations arise. This is where integrated compliance platforms such as https://xpath.global/ become valuable, enabling real-time monitoring and automated risk alerts.

Ultimately, payroll compliance in cross-border remote work scenarios is not a back-office function—it is a frontline compliance issue. Failure to manage it effectively can result in penalties, reputational damage, and strained relationships with both employees and tax authorities.

Employment Law and Immigration Challenges

While tax and payroll issues often dominate discussions around cross-border remote work compliance, employment law and immigration risks are equally critical—and often less visible until problems arise.

From an employment law perspective, the primary challenge lies in determining which country’s laws apply to a remote worker. Even when an employment contract specifies a governing law, local regulations in the host country may override certain provisions. Many jurisdictions enforce mandatory employment protections, including minimum wage requirements, working time rules, termination protections, and collective bargaining rights.

This creates a scenario where employers may unknowingly become subject to foreign employment regimes simply because an employee is working remotely from that location. For example, an employee working from an EU country may gain access to protections under local labour law, regardless of the contractual framework agreed upon in their home country.

Worker classification adds another layer of risk. Misclassifying employees as independent contractors—especially in cross-border contexts—can lead to significant legal and financial consequences. Authorities are increasingly scrutinizing such arrangements, particularly where remote work blurs the line between employment and independent services.

Immigration compliance further complicates the landscape. Contrary to common assumptions, remote work is not always permitted under standard tourist or business visitor visas. Many jurisdictions consider any form of productive work—regardless of employer location—as requiring appropriate work authorization. This means employees working remotely from another country, even for short periods, may be in violation of immigration laws.

The distinction between business visitors and workers is particularly important. Activities such as attending meetings or training sessions may be permitted under business visitor status, but performing core job functions typically is not. Failure to comply with these rules can result in fines, entry bans, or broader reputational risks for the employer.

To navigate these challenges, companies must adopt a holistic compliance approach that integrates employment law and immigration considerations into their remote work policies. Solutions like https://xpath.global/ help organizations assess jurisdiction-specific requirements, manage documentation, and ensure that employee mobility aligns with legal constraints.

Data, Tracking, and Compliance Infrastructure in Cross-Border Remote Work Compliance

As regulatory scrutiny intensifies, cross-border remote work compliance is becoming increasingly dependent on data accuracy, real-time visibility, and system integration. Without a robust infrastructure to track where employees are working and for how long, even the most carefully designed compliance policies will fail in practice.

At the center of this challenge is employee location tracking. Organizations must be able to determine, with precision, the jurisdiction in which work is physically performed. This is not simply an HR concern—it directly impacts tax nexus, payroll obligations, social security exposure, and immigration compliance. However, collecting and processing this data introduces its own set of legal considerations, particularly under frameworks such as the General Data Protection Regulation (GDPR).

Under GDPR, employee location data is considered personal data and must be processed lawfully, transparently, and for a specific purpose. Employers must establish a clear legal basis—typically legitimate interest or legal obligation—while ensuring proportionality and minimizing intrusion. Overly invasive tracking methods can expose organizations to privacy violations, creating a compliance paradox where solving one risk introduces another.

To address this, companies are increasingly implementing structured tracking mechanisms, including:

-

🔸Employee self-declaration systems

-

🔸Automated travel and login monitoring tools

-

🔸Integration with payroll and HR systems

-

🔸Pre-approval workflows for cross-border work

Equally important is the creation of audit trails. Regulators are no longer satisfied with retrospective explanations—organizations must demonstrate that they had proactive controls in place. This includes documenting decision-making processes, risk assessments, and approvals related to cross-border work arrangements.

Technology platforms are playing a pivotal role in enabling this level of control. Solutions such as https://xpath.global/ provide centralized dashboards that combine employee mobility data with jurisdiction-specific compliance rules. These platforms can flag risks in real time—for example, when an employee approaches a tax threshold or enters a jurisdiction with strict employment laws—allowing organizations to act before exposure materializes.

Another critical element is interdepartmental integration. Cross-border remote work compliance cannot be managed in silos. Tax, HR, legal, payroll, and IT functions must operate within a unified framework, supported by shared data and aligned governance structures. Without this integration, gaps inevitably emerge—often in areas that are not immediately visible.

Ultimately, compliance infrastructure is no longer a back-end support function. It is a strategic enabler, allowing organizations to scale remote work policies while maintaining control over complex, multi-jurisdictional risks.

10 Powerful Strategies for Cross-Border Remote Work Compliance

Effectively managing cross-border remote work compliance requires more than reactive fixes—it demands a structured, forward-looking strategy. Below are ten powerful approaches that leading organizations are adopting to mitigate risk while enabling workforce flexibility.

Establish a Centralized Global Mobility Policy

A unified policy creates consistency across jurisdictions and ensures that all cross-border work arrangements are subject to standardized rules and approval processes.

Implement Pre-Approval Frameworks

Employees should not independently decide to work from another country. Pre-approval systems allow organizations to assess legal, tax, and immigration risks before exposure occurs.

Conduct Jurisdiction-Specific Risk Assessments

Each country presents unique risks. Companies must evaluate thresholds for tax, payroll, and employment law on a case-by-case basis.

Define Risk Tiers for Remote Work Scenarios

Categorizing arrangements (e.g., low-risk short stays vs high-risk long-term presence) allows for proportionate compliance measures.

Limit High-Risk Activities in Certain Jurisdictions

Restricting activities such as contract negotiation or revenue generation can reduce permanent establishment exposure.

Align Tax, HR, and Legal Functions

Cross-border remote work compliance requires coordinated decision-making. Fragmented approaches lead to gaps and inconsistencies.

Deploy Real-Time Tracking and Monitoring Tools

Accurate data is essential. Platforms like https://xpath.global/ enable organizations to monitor employee movements and trigger compliance actions proactively.

Standardize Documentation and Audit Processes

Maintaining clear records of approvals, risk assessments, and employee declarations strengthens audit readiness and reduces regulatory exposure.

Leverage External Expertise and Advisory Networks

Given the complexity of multi-jurisdictional rules, partnering with specialized providers ensures access to up-to-date regulatory insights.

Continuously Update Policies Based on Regulatory Developments

As highlighted by the OECD’s evolving guidance, this area is dynamic. Policies must be regularly reviewed and adapted to remain compliant.

These strategies are most effective when implemented as part of a cohesive governance framework, rather than isolated initiatives. The goal is not to eliminate cross-border remote work, but to enable it safely and sustainably.

Governance, Documentation, and Audit Readiness

The final—and often निर्ण—pillar of cross-border remote work compliance is governance. Without strong internal controls and documentation standards, even well-designed policies and systems can fail under regulatory scrutiny.

Governance begins with clear ownership. Organizations must define who is responsible for approving, monitoring, and enforcing cross-border work arrangements. This typically involves a combination of global mobility teams, tax departments, HR, and legal functions. However, responsibility must be clearly delineated to avoid ambiguity and accountability gaps.

A key component of governance is the establishment of internal control frameworks. These include:

-

🔸Approval hierarchies for cross-border work requests

-

🔸Defined escalation procedures for high-risk scenarios

-

🔸Periodic compliance reviews and audits

-

🔸Integration with enterprise risk management systems

Documentation plays a critical role in demonstrating compliance. Authorities increasingly expect companies to provide evidence of:

-

🔸Risk assessments conducted prior to employee relocation

-

🔸Justification for decisions made

-

🔸Monitoring of employee presence and activities

Failure to produce such documentation can result in adverse outcomes, even if the underlying compliance position is defensible.

Audit readiness also requires organizations to anticipate multi-jurisdictional inquiries. It is not uncommon for tax authorities, labour inspectors, and immigration officials in different countries to examine the same employee arrangement from their respective perspectives. This makes consistency in documentation and reporting essential.

Digital platforms such as https://xpath.global/ support this process by centralizing data, maintaining audit trails, and ensuring that documentation is accessible and aligned across functions. This reduces the administrative burden while strengthening the organization’s ability to respond to regulatory challenges.

In a landscape defined by increasing enforcement and complexity, governance is not merely a control mechanism—it is a competitive advantage. Companies that can demonstrate structured, transparent, and well-documented compliance frameworks are better positioned to navigate regulatory scrutiny and sustain flexible workforce models.

Conclusion

The evolution of cross-border remote work compliance marks a fundamental shift in how organizations must approach workforce mobility. What was once an operational or HR-driven flexibility initiative has now become a multi-dimensional legal and regulatory challenge—touching tax, payroll, employment law, immigration, and data protection simultaneously.

As highlighted by the OECD’s 2026 consultation and increasing enforcement trends worldwide, regulators are no longer treating remote work as an exception. Instead, they are adapting existing frameworks to ensure that economic activity—regardless of where it occurs—is properly taxed and regulated. This creates a landscape where even seemingly low-risk arrangements can trigger significant compliance obligations.

The key takeaway for organizations is clear: reactive compliance is no longer sufficient. Businesses must move toward proactive, data-driven governance models that allow them to anticipate risks before they materialize. This requires not only strong internal policies and cross-functional alignment but also the adoption of technology solutions that provide real-time visibility into employee activity across jurisdictions.

Platforms like https://xpath.global/ are increasingly becoming essential in this ecosystem, enabling companies to centralize compliance processes, automate risk detection, and maintain audit-ready documentation. However, technology alone is not enough. Success in this space depends on a combination of legal expertise, operational discipline, and strategic foresight.

Ultimately, organizations that invest in robust cross-border remote work compliance frameworks will not only mitigate risk—they will gain a competitive advantage. They will be better positioned to attract global talent, respond to evolving work patterns, and operate confidently in a fragmented regulatory environment.

In a world where work is no longer tied to a single location, compliance must be equally flexible—but far more precise.

FAQs

What is cross-border remote work compliance?

Cross-border remote work compliance refers to the process of ensuring that employers meet all legal, tax, payroll, employment, and immigration obligations when employees work from a country different from their primary place of employment.

Can remote employees create a permanent establishment risk?

Yes, employees working remotely in another country can create permanent establishment (PE) risk, particularly if they perform core business activities, conclude contracts, or operate from a fixed location over time.

Do employers need to run payroll in another country for remote workers?

In many cases, yes. Employers may be required to register for local payroll, withhold taxes, or implement shadow payroll depending on the duration and nature of the employee’s presence.

How does remote work impact employee tax residency?

Employees may become tax residents in another country based on physical presence, center of vital interests, or other local rules, potentially leading to dual residency and complex tax obligations.

Is immigration permission required for remote work?

Often, yes. Many countries consider remote work as “work activity,” requiring proper visas or permits—even if the employer is based in another jurisdiction.

How can companies manage cross-border compliance effectively?

Organizations can manage compliance by implementing centralized policies, using tracking technology, conducting risk assessments, and leveraging platforms like https://xpath.global/ for integrated compliance management.

Are short-term remote work arrangements low risk?

Not necessarily. Even short-term arrangements can trigger payroll, tax, or immigration obligations depending on the jurisdiction and nature of the work performed.